When people hear the phrase “insider trading,” it usually sparks images of corporate executives sneaking around with secret information or Wall Street traders making millions illegally. While those images aren’t entirely false, the truth about insider trading in the U.S. is far more complex. It is not always illegal, and in fact, some forms of insider trading are perfectly lawful when properly disclosed. However, illegal insider trading remains one of the most serious securities violations in the country, drawing the attention of regulators, lawmakers, and investors alike.

This article will break down what insider trading really means, why it matters, how it is regulated in the U.S., some of the most famous cases in history, and what the future may look like for insider trading laws.

What Is Insider Trading?

At its most basic definition, insider trading refers to buying or selling a publicly traded company’s stock or other securities based on material, non-public information. “Material” means information that a reasonable investor would consider important in making a decision to buy, sell, or hold a security. “Non-public” means the information has not been widely disseminated to the general investing public.

For example, if a company executive knows that their firm is about to announce a major merger, and they buy shares before that news becomes public, that could constitute illegal insider trading. When the merger is announced and the stock price jumps, they make a profit at the expense of investors who didn’t have the same information.

Legal vs. Illegal Insider Trading

It may surprise some people to learn that not all insider trading is unlawful. In fact, insiders such as CEOs, CFOs, directors, and other executives are often significant shareholders in their companies. They buy and sell stock in their own firms all the time. This activity is legal as long as they report their transactions to the Securities and Exchange Commission (SEC) and avoid trading based on confidential information.

The key distinction comes down to timing and disclosure. If an insider trades on material information that has not yet been made public, that is illegal. If they trade after the information has been made public and follow disclosure rules, it is legal.

To ensure transparency, the SEC requires insiders to file forms (like Form 4) within a short period after making a trade. These filings are available to the public, meaning ordinary investors can see when insiders are buying or selling shares.

Why Insider Trading Matters

Illegal insider trading undermines the integrity of financial markets. The U.S. stock market operates on the principle that all investors should have equal access to material information. If some investors profit by exploiting secrets, it creates an uneven playing field and erodes trust in the market.

For retail investors, this can be discouraging. Imagine buying shares at the same time an executive is secretly dumping them because they know bad news is coming. When the stock falls, the insider walks away with millions saved, while the average investor shoulders the loss. That imbalance is exactly what regulators aim to prevent.

In addition, insider trading can reduce overall market efficiency. Markets work best when prices reflect all available information. If critical information is kept hidden by insiders until after they trade, stock prices do not reflect reality, which distorts valuations and reduces investor confidence.

How Insider Trading Is Regulated in the U.S.

The Securities and Exchange Commission (SEC) is the primary regulator of insider trading in the U.S. The SEC enforces laws that prohibit corporate insiders and others with access to confidential information from unfairly profiting in the securities markets.

Key laws and regulations include:

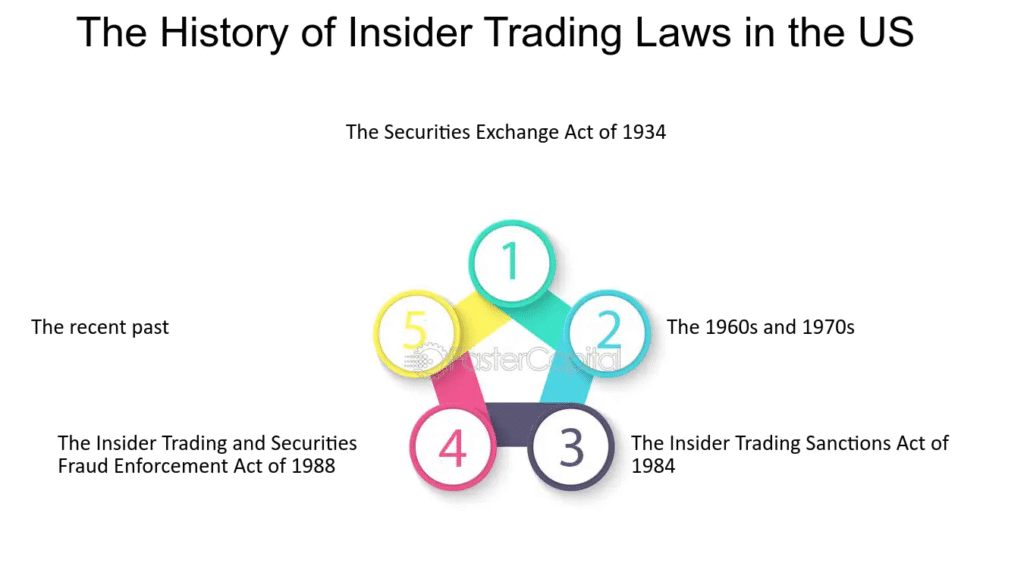

- The Securities Exchange Act of 1934: This act established the SEC and gave it authority to regulate securities trading, including insider trading.

- Rule 10b-5: This is the most important rule governing insider trading. It prohibits fraud, misrepresentation, and deceit in connection with the purchase or sale of securities.

- The Insider Trading Sanctions Act of 1984: This law increased penalties for insider trading, including allowing fines up to three times the profits gained or losses avoided.

- The Insider Trading and Securities Fraud Enforcement Act of 1988: This strengthened the SEC’s ability to prosecute insider trading cases and imposed greater liability on employers who failed to prevent violations.

The Department of Justice (DOJ) also prosecutes insider trading criminally, meaning violators can face prison sentences in addition to fines.

Famous Insider Trading Cases in the U.S.

Insider trading scandals have been a recurring theme in American financial history, often involving high-profile names. A few examples stand out:

- Ivan Boesky (1980s): Perhaps the most infamous insider trading case of the 1980s, Boesky, a Wall Street arbitrageur, made hundreds of millions of dollars trading on insider information. He was fined and served prison time, and his case inspired the movie Wall Street.

- Martha Stewart (2001): The lifestyle mogul was convicted of obstruction of justice and lying to investigators in a case tied to insider trading involving the biotech company ImClone. While she was not convicted of insider trading itself, the case highlighted how even celebrities can face consequences for suspicious trades.

- Raj Rajaratnam (2009): The billionaire hedge fund manager was convicted of orchestrating one of the largest insider trading schemes in U.S. history, involving numerous corporate insiders and analysts. He received an 11-year prison sentence, one of the harshest ever for insider trading.

These cases illustrate how insider trading can cut across industries, from finance to healthcare to consumer brands.

Gray Areas and Modern Challenges

Insider trading law is not always crystal clear. Many cases revolve around whether the information was truly “material” and whether the trader had a “duty” to keep it confidential. Courts have struggled with cases where the information was indirectly obtained or where “tippees” (those who receive tips from insiders) made trades.

In the modern era, insider trading enforcement faces new challenges. With the rise of digital communication, it has become easier to share sensitive information quickly. Social media platforms, encrypted messaging apps, and anonymous forums can all facilitate the spread of confidential information.

Another area of controversy involves political insider trading. Members of Congress and their staff often have access to non-public information about upcoming legislation that could affect stock prices. While there are laws like the STOCK Act of 2012 aimed at curbing this, enforcement has been inconsistent, and public skepticism remains high.

The Future of Insider Trading Regulation

Looking ahead, insider trading laws in the U.S. are likely to evolve further. Some legal scholars argue for clearer statutory definitions of what constitutes insider trading to reduce ambiguity in prosecutions. Others believe harsher penalties are necessary to deter would-be violators.

Technology will also play a major role. Regulators are increasingly using data analytics, artificial intelligence, and machine learning to detect suspicious trading patterns. These tools can analyze millions of trades in real time and flag activity that may warrant investigation.

For investors, the best takeaway is to understand that while markets strive for fairness, they are not immune to abuse. Awareness of insider trading risks can help investors approach the market more cautiously and evaluate companies with a critical eye.

Conclusion

The truth about insider trading in the U.S. is that it is not a simple matter of legal versus illegal trades. Some insider trading is routine and lawful, while other forms are manipulative and criminal. What matters most is whether trades are based on material, non-public information that gives insiders an unfair advantage.

Illegal insider trading threatens the fairness and integrity of U.S. markets, undermines investor confidence, and carries severe legal consequences. Through decades of legislation, enforcement, and high-profile cases, the U.S. has built a strong regulatory framework. Yet as markets and technology evolve, so too must the laws and tools used to keep them fair.