The stock market has always been filled with patterns, cycles, and anomalies that investors study to gain an edge. One of the most widely discussed seasonal anomalies is the January Effect. Traditionally, this refers to the tendency of U.S. stock prices, particularly small-cap stocks, to rise more than usual during the month of January. For decades, the phenomenon influenced investment strategies, with many traders adjusting their portfolios to capitalize on the expected gains.

But the big question remains: does the January Effect still exist in U.S. stocks today, or has it faded with time? Let’s explore the history, reasons behind the effect, recent market behavior, and what it means for modern investors.

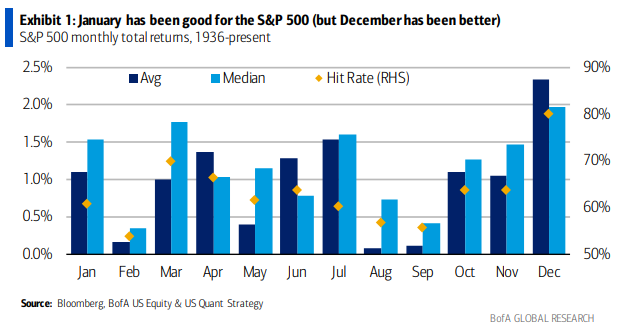

Understanding the January Effect

The January Effect is rooted in the idea that stock prices, especially those of smaller companies, often see a noticeable increase during January compared to other months. The concept dates back to the mid-20th century when analysts observed that stocks, on average, delivered higher-than-usual returns at the beginning of the year.

This seasonal boost was particularly noticeable in small-cap stocks, which typically outperformed large-cap stocks in January. The effect was so strong that many believed it was nearly predictable, making it a cornerstone of certain trading strategies.

Why Did the January Effect Occur?

There are several theories explaining why the January Effect took hold in U.S. markets:

- Tax-Loss Selling: Investors often sell losing positions in December to offset capital gains taxes. Once the new year begins, they reinvest that money, often back into the same or similar stocks, creating a demand surge in January.

- Window Dressing: Institutional investors, such as mutual funds, frequently sell underperforming stocks before year-end to make portfolios look more attractive on reports. In January, they rebalance by buying back those same stocks.

- Year-End Bonuses and New Cash Flows: Many investors receive bonuses or allocate new funds to retirement accounts at the start of the year, leading to increased buying activity.

- Behavioral Psychology: Investors tend to start the year with optimism and fresh strategies, contributing to stronger early-year momentum.

These combined factors historically created upward pressure on stock prices in January, especially among undervalued or overlooked smaller companies.

Historical Evidence of the January Effect

Research during the 1970s and 1980s strongly supported the January Effect. For example, studies showed that small-cap stocks often delivered outsized gains in the first few trading days of January, sometimes enough to account for a large portion of their annual return.

Wall Street even had a popular saying: “As goes January, so goes the year.” This belief suggested that a positive January often signaled a positive year for the broader stock market.

During this period, investors actively designed strategies around the January Effect, expecting it to consistently generate above-average returns.

Has the January Effect Disappeared?

In more recent decades, the January Effect appears to have weakened significantly. Several reasons explain why:

- Market Efficiency: With greater awareness of the anomaly, investors started anticipating the effect, buying earlier (in December) and reducing the actual impact seen in January.

- Changes in Tax Rules: Adjustments in U.S. tax laws and investor behavior over the years have made tax-loss selling less concentrated at year-end.

- Rise of Institutional Investors: Today’s markets are dominated by institutions with sophisticated algorithms and strategies. Their influence reduces seasonal anomalies that were more visible in retail-driven markets.

- Global Capital Flows: With globalization and international investing, U.S. stock market trends are now influenced by broader global factors, making localized anomalies less impactful.

For instance, data from the last two decades shows that while January returns are sometimes strong, the consistent, predictable outperformance that defined the January Effect is no longer present. Some years even saw negative returns in January, challenging the idea that the effect is still reliable.

What Do Recent Studies Say?

Modern studies suggest that while the January Effect may not be as powerful as before, certain remnants still exist. Small-cap stocks occasionally outperform in January, but the magnitude is smaller, and the effect is inconsistent.

A 2020 analysis of U.S. stock performance revealed that January returns were no longer statistically different from other months for most sectors. However, niche areas of the market—such as micro-cap stocks or thinly traded securities—sometimes still experience seasonal January boosts, likely due to lingering behavioral and tax-related influences.

The Role of Behavioral Finance

Even though markets are more efficient today, behavioral finance suggests that investor psychology can still drive seasonal effects. Optimism at the start of the year, combined with portfolio reshuffling, can occasionally create upward momentum in January.

However, this doesn’t guarantee the widespread, predictable January rallies of the past. Instead, any effect is more likely to be subtle, temporary, and dependent on market conditions such as interest rates, economic outlook, and investor sentiment.

Does the January Effect Still Matter for Investors?

For long-term investors, the January Effect has little impact. Successful investing is built on fundamentals, diversification, and patience—not on seasonal anomalies. Chasing patterns like the January Effect can lead to overtrading and disappointment.

That said, active traders and hedge funds still monitor seasonal trends. Even a small bias in January could present short-term trading opportunities in specific market segments, particularly among small-cap or underfollowed stocks.

But investors should treat it as a potential seasonal tailwind, not a guaranteed strategy. The risks of relying on outdated market myths often outweigh the benefits.

The Bigger Picture: Market Myths and Realities

The story of the January Effect illustrates a broader truth about financial markets: once an anomaly becomes widely known, it tends to disappear. Markets evolve, participants adapt, and inefficiencies are arbitraged away.

Today’s U.S. stock market is far more efficient, liquid, and competitive than in the mid-20th century. While seasonal effects may still surface occasionally, they are no longer dependable drivers of performance.

For investors, the key takeaway is clear: focus on long-term fundamentals rather than short-term seasonal strategies. The January Effect may exist in faint traces, but it is no longer the powerful market force it once was.

Final Thoughts

So, does the January Effect still exist in U.S. stocks? The answer is yes, but only faintly and inconsistently. The strong, predictable rallies of the past have faded as markets became more efficient and globalized. While small-cap stocks and certain niches may still experience January bumps, they are far less reliable than before.