Every four years, as the United States heads into a presidential election, Wall Street gears up for uncertainty. Investors, analysts, and the media often speculate about how election outcomes might influence the stock market. But do U.S. elections really drive stock market performance, or is it more of a myth reinforced by headlines? To answer this, we need to examine historical data, investor psychology, economic fundamentals, and political trends.

The Link Between Politics and Market Sentiment

Markets are influenced by expectations. During an election season, investors pay close attention to candidates’ policies on taxes, trade, regulation, healthcare, and foreign relations. For example, a candidate promising corporate tax cuts may fuel optimism in equity markets, while another proposing higher regulations on specific industries could create nervousness among investors in those sectors.

However, much of this is sentiment-driven. Markets price in expectations quickly, often before the election even happens. This means the anticipation of policy shifts can move markets more than the actual results.

Historical Patterns in Election Years

When we look at the historical performance of the U.S. stock market during election years, some interesting patterns emerge.

- The S&P 500 tends to experience higher volatility in election years compared to non-election years.

- On average, the stock market has delivered positive returns in most election years, though the gains are often below long-term averages.

- Markets generally perform better in the year following an election, as uncertainty is resolved and policy clarity emerges.

For example, during the 2008 financial crisis, markets were already collapsing due to economic turmoil, and the election itself did little to alter the trajectory. On the other hand, in 2016, markets dipped sharply on election night when it became clear Donald Trump would win, but quickly rebounded and rallied for months afterward.

This shows that while elections may temporarily shake markets, fundamentals usually reclaim control.

The “Presidential Cycle” Theory

One of the most widely cited ideas is the “Presidential Cycle Theory,” which suggests that U.S. markets follow a predictable pattern across the four years of a presidency. Historically, the first two years of a presidential term have produced weaker stock returns, while the third year tends to deliver the strongest gains. The fourth year, when elections take place, has been moderately positive.

The reasoning is that presidents and policymakers often push unpopular reforms or tough economic measures early in their term, then focus on growth-oriented policies closer to re-election campaigns. While this pattern has held at times, it is not a guarantee and should not be treated as a reliable investment strategy.

Do Political Parties Matter?

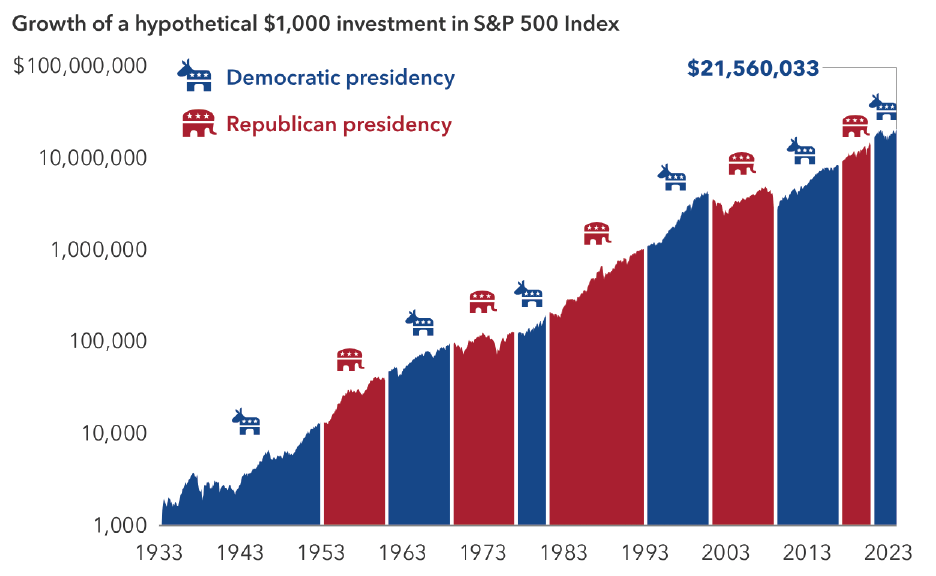

Another common belief is that markets perform better under certain political parties. Historically, U.S. stock markets have shown stronger average returns under Democratic presidents than Republican ones. However, this does not necessarily mean Democratic policies are better for stocks. Economic cycles, global events, and Federal Reserve policies often play a bigger role than which party is in power.

For instance, President Bill Clinton oversaw one of the greatest bull markets in history, but it was largely fueled by the tech boom. Similarly, the strong rally under President Donald Trump was driven by corporate tax cuts and a pre-pandemic economic expansion.

The takeaway? Party affiliation alone is not a reliable predictor of stock market outcomes.

The Role of Policy vs. Fundamentals

While elections can create short-term ripples, long-term stock market performance is driven more by fundamentals such as corporate earnings, economic growth, interest rates, and technological innovation. Elections can influence these indirectly through policies, but they are rarely the primary driver.

Consider healthcare stocks. When Democrats have proposed reforms to lower drug prices or expand public healthcare, shares of pharmaceutical and insurance companies often come under pressure. Yet over the long run, many of these companies adapt, restructure, and continue to grow.

Similarly, clean energy stocks may benefit when a candidate prioritizes climate change initiatives, while traditional energy companies may gain under a more fossil-fuel-friendly administration. But again, broader global demand, innovation, and market forces often outweigh policy shifts.

Investor Psychology and Volatility

Elections amplify uncertainty, and uncertainty breeds volatility. Many investors choose to stay on the sidelines or reduce risk exposure during election years. This can exaggerate market moves, especially when polls are tight or unexpected events occur.

For example, the 2000 election between George W. Bush and Al Gore led to weeks of market turbulence as the outcome remained undecided due to recounts. Similarly, Brexit in the U.K., though not a U.S. election, demonstrated how political events can send shockwaves through global markets.

The key for investors is to recognize that volatility during elections is often temporary. Once the results are clear and policy directions are understood, markets typically stabilize.

Should Investors Time the Market Around Elections?

Many investors wonder whether they should change their strategy during election years. History suggests that trying to time the market based on elections is risky. Short-term market moves are unpredictable, and sitting on the sidelines can mean missing out on gains.

Instead, a long-term perspective focused on fundamentals and diversification tends to outperform panic-driven decisions. Investors who stayed invested through the uncertainty of past elections generally saw strong returns over time.

Case Studies of U.S. Elections and the Market

- 2012 Election (Obama vs. Romney): Markets remained steady before the election but faced volatility around fiscal policy debates afterward. Long-term, the bull market continued.

- 2016 Election (Trump vs. Clinton): Market futures plunged overnight when Trump won, but quickly reversed as investors anticipated tax cuts and deregulation.

- 2020 Election (Biden vs. Trump): Markets were already recovering from the pandemic-driven crash. Despite uncertainty and contested results, stocks surged on expectations of fiscal stimulus and vaccine rollouts.

These examples highlight that while elections create headlines and short-term swings, they rarely derail broader market trends.

Conclusion: Elections Matter, But Fundamentals Rule

So, do U.S. elections really drive stock market performance? The answer is: only to a limited extent. Elections can increase volatility, shape sector-specific outcomes, and influence short-term sentiment. But in the long run, fundamentals such as earnings growth, innovation, global trade, and Federal Reserve policies have far greater impact on market direction.

For investors, the lesson is clear. Stay informed, understand how policies might affect certain industries, but avoid making drastic portfolio changes solely based on election outcomes. History shows that patience and discipline consistently outperform political speculation.